If they desire to keep the house they must settle the loan balance with a brand-new loan through refinancing or with other money offered to them. If they pick to sell the home, they need to get in touch with the servicer of the reverse home mortgage as quickly as possible and inform them of their decision and preserve excellent communication with that servicer.

Luckily, a reverse mortgage is a non-recourse loan. who has the lowest apr for mortgages. This indicates that if the amount due on the loan, consisting of interest and fees, is greater than the amount the home will cost the heirs/beneficiaries are not responsible for any additional quantity owed. A sale to a bona fide non-related third celebration typically does not have any limitations.

A knowledgeable Probate attorney can help you comprehend your options to deal with a home topic to a reverse mortgage. Contact the Probate attorneys with the Law Offices of Nay & Friedenberg in Portland, Oregon at (503) 245-0894 to set an appointment. If you wish to discover more about estate planning, to receive our FREE Legal/Financial Preparation Guide.

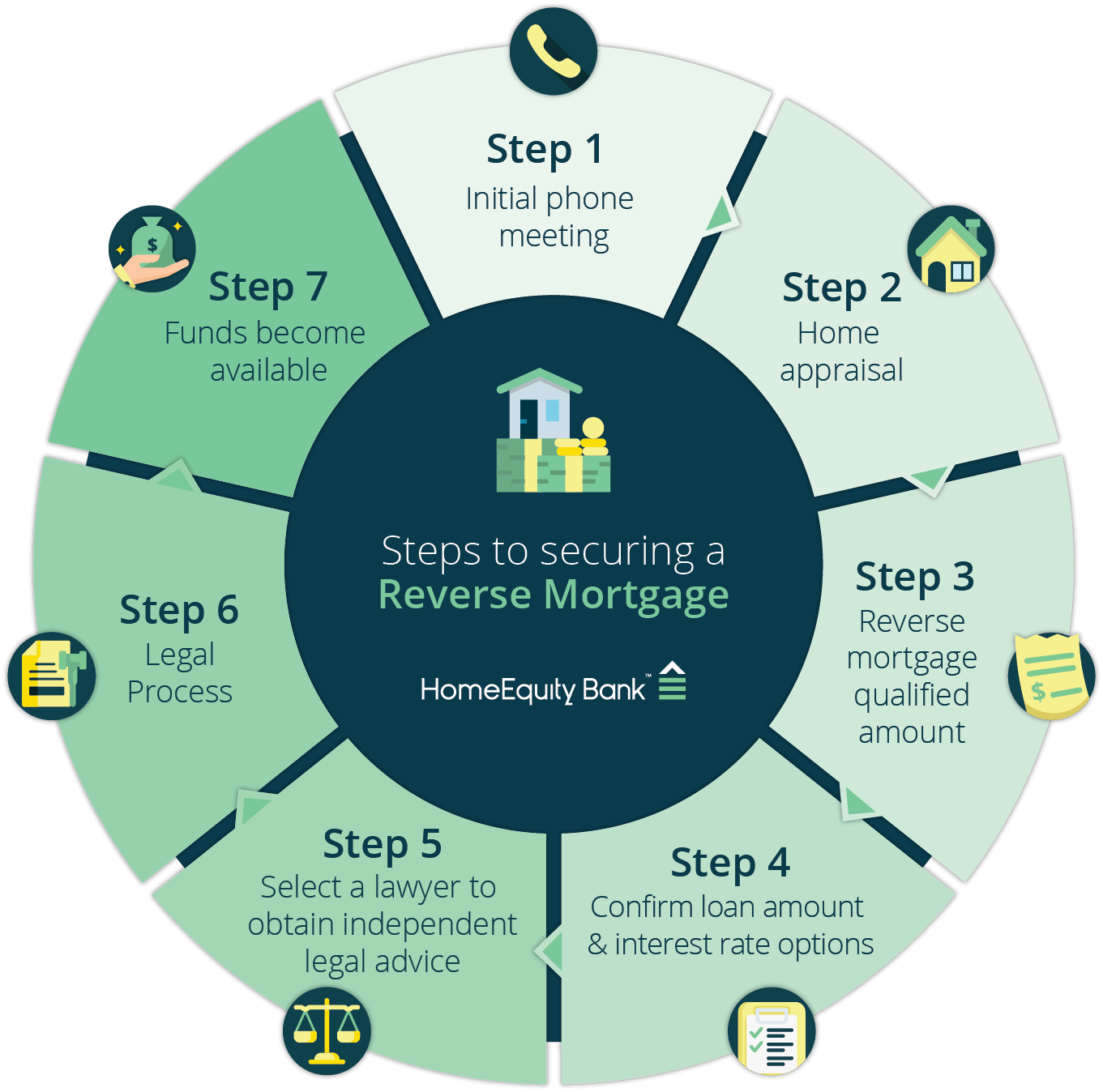

A reverse home mortgage is a mortgage that you do not have to repay for as long as you reside in your home. It can be paid to you in one lump sum, as a routine monthly income, or at the times and in the amounts you want. The loan and interest are paid back just when you sell your house, permanently move away, or die.

They are paid back completely when the last living customer passes away, sells the house, or permanently moves away. Due to the fact that you make no monthly payments, the quantity you owe grows bigger gradually. By law, you can never ever owe more than your home's worth at the time the loan is paid back.

If you stop working to pay these, the loan provider can utilize the loan to make payments or need you to pay the loan in full. All property owners need to be at least 62 years old. A minimum of one owner should live in your home the majority of the year. Single household, one-unit home.

Some condominiums, prepared system advancements or made homes. NOTE: Cooperatives and many mobile houses are not eligible. Reverse home mortgages can be paid to you: All at when in cash As a monthly income As a credit line that lets you choose how much you want and when In any combination of the above The quantity you get usually depends upon your age, your house's worth and area, and the cost of the loan.

The Ultimate Guide To What Are The Main Types Of Mortgages

The majority of people get the most cash from the Home Equity Conversion Home Loan (HECM), a federally guaranteed program. Loans Great site used by some states and local federal governments are typically for specific functions, such as paying for house repair work or real estate tax. These are the least expensive cost reverse home loans. Loans offered by some banks and mortgage business can be utilized for any function.

HECM loans are practically always the least costly reverse mortgage you can get from a bank or mortgage business, and in most cases are considerably less expensive than other reverse home loans. Reverse mortgages are most pricey in the early years of the loan and usually end up being less pricey gradually.

The federal government needs you to see a federally-approved reverse mortgage counselor as part of getting a HECM reverse home mortgage (what do i do to check in on reverse mortgages). To learn more about Reverse Home mortgages, go to AARP: Comprehending Reverse Home Loans.

This question is very typical, so I published the riles after the last homeowner leaves your home. It provides me a chance to describe that this FHA Reverse Home loan has FHA insurance coverage; which means the estate can not be passes a financial obligation. Dealing with an estate after the death of a loved one can be demanding.

If you're the surviving partner, you'll want to know your alternatives and obligations. If you're one of the beneficiaries, you have particular duties and choices you'll need to make. Whether you desire to keep the home or not, you have options. You want to make certain that you comprehend what they are.

If the house deserves more than the loan amount, the beneficiaries may sell the house, settle the loan, and keep the rest of the cash from the sale. Sell the property for 95% of its appraised worth in a short sale to satisfy the loan. Walking away from the home will result in foreclosure and eases any obligation for paying off the loan.

This titles the residential or commercial property back to the lender. This permits the house to go into reverse home mortgage foreclosure and offers the seller the property to please the loan. Reverse Mortgage After Death Timeline Here's a timeline of what to expect to handle a reverse home loan after death. Within 1 month of getting notification of the death of the debtor, the loan servicer will send out a due and payable notice to the estate, along with info on the reverse loan and the eligibility requirements for a deferral duration of the reverse home mortgage after death.

The Only Guide for Individual Who Want To Hold Mortgages On Homes

Furthermore, the mortgagees should obtain an appraisal of the home no behind one month after the due and payable notification is sent. The enduring, non-borrowing partner may request a deferment if they meet the requirements. Throughout this time, the estate can sell your home, or otherwise satisfy the loan.

Within 6 months of the death of the last how to legally get out of timeshare contract making it through debtor, the loan servicer might begin foreclosure proceedings if someone does not pay the loan quantity. If a deferment has been provided, then the foreclosure proceedings may start 6 months after the end of the deferral. The estate might request 2 extensions in 3-month periods.

When one spouse passes away, however the surviving partner is a borrower on the reverse home loan, the terms of the loan do not alter. Also, the enduring spouse might continue to live in the house. If the surviving spouse is not a borrower, then the mortgagee will send out a letter specifying the requirements for a deferral duration before the loan is due and payable.

Otherwise, a notice that the loan is due and payable will be provided. As soon as receiving a notification that the loan is due and payable, the partner might select to sell the house, hand las vegas timeshare resorts the home over to the lender, or keep the home by paying the reverse loan quantity. During the time after the death of the debtor, the spouse must preserve the residential or commercial property and pay real estate tax.

This might cause foreclosure on the home. Successors' Duty for the Reverse Home Loan After Death of the Debtor After the death of the debtor, the successors will receive a letter from the loan servicer. The letter will offer info on the customer's estate, information on the reverse mortgage, and available choices for satisfying the loan.

Here's some suggestions for kids of senior citizens for managing the reverse mortgage after death. To keep the home, the loan must be settled. The expense to pay off the loan is never ever more than 95% of the assessed worth of the home, even if the loan amount is more.